First Seen

2023-12-17T06:02:11+00:00

simple-description (qwen3.5_2b-q8_0)

The meme argues that the current rise in mortgage rates is a direct repeat of the "Volcker disinflation" event in 1979, where high interest rates triggered a massive housing bubble and subsequent crash. The chart illustrates that historically, when rates spike (represented by the dark blue and light blue lines), the housing market experiences a rapid burst followed by a severe downturn. The 2021 data (red line) mirrors this boom-and-bust cycle, suggesting that despite recent "inflation" fears, the fundamental dynamics of the housing market remain stuck in historical patterns of destructive financial cycles.

simple-description (llama3.2-vision_11b)

The meme is a graph showing the average annual increase in US housing prices from 1970 to 2020, with a red line indicating the current year. The graph shows a significant increase in housing prices, with a steep incline in recent years. The meme is likely commenting on the high cost of housing and the struggle for affordability, with the caption "We're all just trying to afford a house" implying that the rising cost of housing is a major concern for many people.

detailed-analysis (gemma3-27b-vision)

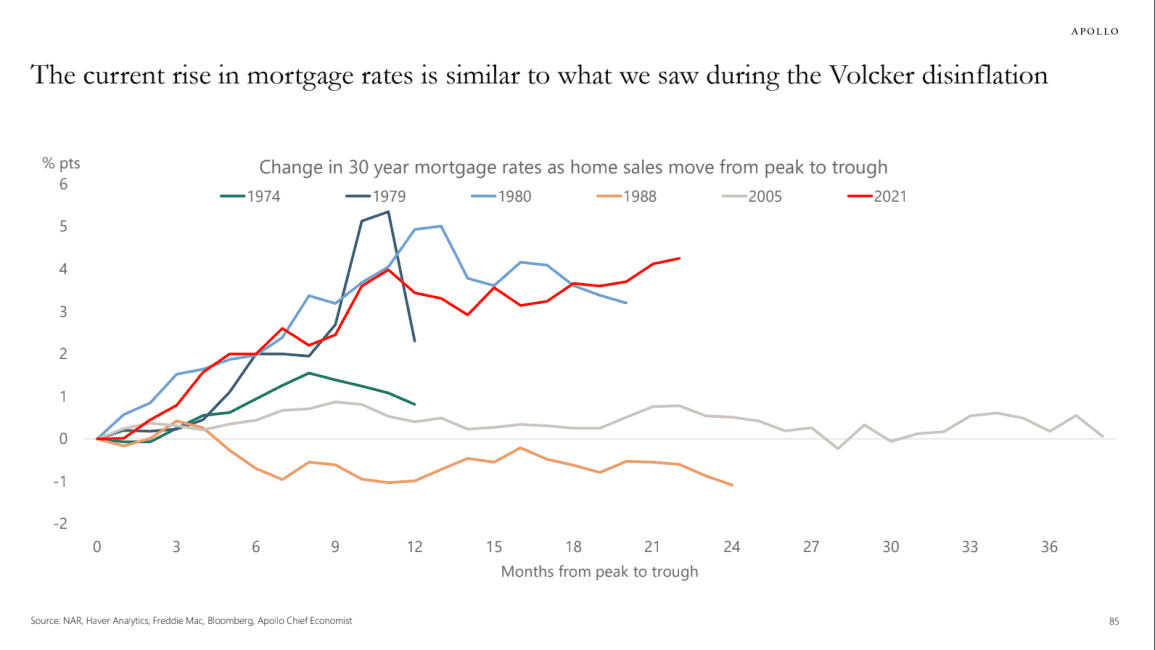

Okay, let's break down this graph through several theoretical lenses, noting that some lenses will be more applicable (and insightful) than others.

Visual Description

The graph depicts the change in 30-year mortgage rates (in percentage points) over the period from the peak to the trough of home sales for five different periods: 1974, 1979, 1980, 1988, 2005 and 2021. The x-axis represents the number of months from peak to trough, ranging from 0 to 36. The y-axis ranges from -1 to 6 percentage points.

Key observations:

- 1974 & 1979: Show relatively modest and quick shifts in rates, with increases followed by stabilization around the 1-2% level.

- 1980: Exhibits a sharp increase in rates, peaking around 4-5%, followed by a steep decline, suggesting a forceful intervention or policy shift.

- 1988: Shows a small increase in rates followed by flatlining.

- 2005: A slight dip in rates followed by a very slow decrease.

- 2021: Shows a swift increase in rates, reaching around 3% in around 9 months, and then tapering off. This mirrors, to a degree, the 1980 curve.

- Overall: The graph emphasizes how mortgage rate changes respond to the cycle of home sales. There is a clear peak to trough pattern, with different periods showing distinct responses, and 2021 drawing parallels to the Volcker disinflation period of 1980.

Foucauldian Genealogical Discourse Analysis

This graph is not merely a neutral depiction of economic data; it’s a product of discourses around homeownership, finance, and monetary policy. A Foucauldian analysis examines how these discourses constitute our understanding of the economy and regulate behavior.

- Power/Knowledge: The graph embodies a "power/knowledge" relationship. Economic indicators like mortgage rates are presented as objective truths ("knowledge"), but their selection and presentation are shaped by institutions with power (e.g., Freddie Mac, Bloomberg). This creates a specific regime of truth about housing and finance.

- Discipline & Normalization: The graph implicitly reinforces norms around homeownership as a desirable goal and stable investment. The focus on rates as a measure of "health" disciplines individuals to conform to the logic of the housing market. The notion that rates must be managed within certain bounds (the visible pattern) is a form of normalization.

- Genealogy of "Stable" Rates: Tracing the history of how "stable" mortgage rates became a desirable outcome reveals that this isn’t a natural state, but a socially constructed one. The graph implicitly relies on the historical genealogy of concepts like "inflation," "monetary policy," and “affordable housing,” all of which are subject to shifting definitions and power dynamics.

- The "Volcker Disinflation" as Framing: The framing of the current situation as similar to the Volcker period is a significant act of discourse. It invokes a specific historical narrative (Volcker's aggressive policy to curb inflation) and implicitly suggests a parallel course of action. It positions the current situation within a pre-existing understanding of economic history.

Critical Theory

Using a Critical Theory approach, we can examine the inherent power dynamics and systemic issues that shape the depicted trends.

- Commodification of Housing: The graph is built on the premise that housing is a commodity subject to market forces. Critical Theory questions the inherent social injustice of treating shelter as a commodity, potentially excluding those unable to participate in the market. The rate fluctuations directly impact access to this essential need.

- Capital Accumulation: The constant focus on mortgage rates and housing prices serves the larger project of capital accumulation. The graph implicitly supports a system where financial institutions and investors profit from the housing market, potentially at the expense of home buyers and communities.

- Ideology of Homeownership: The graph reinforces the dominant ideology of homeownership as the "American Dream." This ideology masks the structural inequalities that make homeownership inaccessible to many, and perpetuates a system where wealth is concentrated in the hands of a few.

- Systemic Risk: The sharp increases and decreases in rates (particularly in 1980 and 2021) hint at the systemic risks inherent in the housing market. Critical Theory emphasizes the need to address these risks to prevent financial crises and protect vulnerable populations.

Marxist Conflict Theory

Applying a Marxist lens, we can interpret the graph as a manifestation of class struggle and the inherent contradictions of capitalism.

- Capital vs. Labor: The fluctuations in mortgage rates represent the conflict between capital (financial institutions and investors) and labor (home buyers). Capital seeks to maximize profits through interest rates, while labor seeks affordable housing.

- Exploitation of Rent: Mortgage payments, including interest, can be seen as a form of rent (or surplus value) extracted from the working class. The graph highlights how this rent fluctuates based on market conditions.

- Housing as a Site of Class Reproduction: The graph implicates housing as a key mechanism for reproducing class inequalities. Those with wealth can readily access homeownership and build equity, while those without face ongoing financial hardship.

- Crisis Tendency: The sharp spikes in rates, and the potential for financial instability they represent, can be interpreted as a manifestation of capitalism's inherent tendency towards crisis.

Postmodernism

A postmodern reading of the graph challenges the notion of objective truth and emphasizes the constructed nature of reality.

- Rejection of Grand Narratives: Postmodernism rejects grand narratives like the "American Dream" or the idea that stable housing is a universal goal. It questions the underlying assumptions that inform the graph.

- Deconstruction of "Stability": The concept of "stable" mortgage rates is deconstructed as a socially constructed ideal. It is not a natural state, but a product of power relations and discourse.

- Emphasis on Fragmentation: The different curves in the graph reflect the fragmentation of the housing market and the diversity of experiences.

- Simulacra and Simulation: The graph itself is a simulacrum – a representation of reality that has become detached from the real. It is a mediated experience that shapes our understanding of the housing market.

Queer Feminist Intersectional Analysis (Less Directly Applicable, but Potential Insights)

While less central than the other lenses, a Queer Feminist Intersectional analysis could illuminate how inequalities in housing access are compounded by intersecting identities.

- Gendered Impacts: Mortgage approval rates and housing affordability often disproportionately impact women, particularly single mothers and women of color. A Queer Feminist lens would examine how gender norms and economic inequalities contribute to these disparities.

- Racial Discrimination: Historical and ongoing racial discrimination in housing (e.g., redlining, lending practices) creates significant barriers to homeownership for people of color. Intersectional analysis would examine how race intersects with gender, class, and other identities to exacerbate these disparities.

- LGBTQ+ Exclusion: LGBTQ+ individuals may face discrimination in housing and lending, and may also experience unique challenges related to family structures and legal rights.

- Deconstruction of the "Ideal" Homeowner: The graph implicitly assumes a particular image of the "ideal" homeowner (heteronormative, middle-class, etc.). A Queer Feminist analysis would challenge this assumption and advocate for more inclusive housing policies.

In conclusion: This graph, while seemingly straightforward, is rich with potential meanings when viewed through various theoretical lenses. Each perspective reveals different layers of power, inequality, and social construction. It demonstrates how seemingly objective data is always embedded in a complex web of social, economic, and political forces.

tesseract-ocr

Aroto The current rise in mortgage rates is similar to what we saw during the Volcker disinflation % pts Change in 30 year mortgage rates as home sales move from peak to trough ® mm 974 om 979 —1980 ——1988 2005 —2021 5 aa 4 3 2 1 : ST ee ES 1 -2 oO 3 6 9 12 15 18 21 24 27 30 33 36 Months from peak to trough Sauce NAR vr yc de Mx, amb, ple cor 's

simple-description (llama3.2-vision)

The meme is a graph comparing the current inflation rate to previous inflation rates, with the current rate being significantly higher. The graph is titled "The current inflation rate is not like the past" and features a quote from a 2023 article stating "The current inflation rate is not like the past, it is like 1980."