First Seen

2023-12-17T06:02:28+00:00

simple-description (qwen3.5_2b-q8_0)

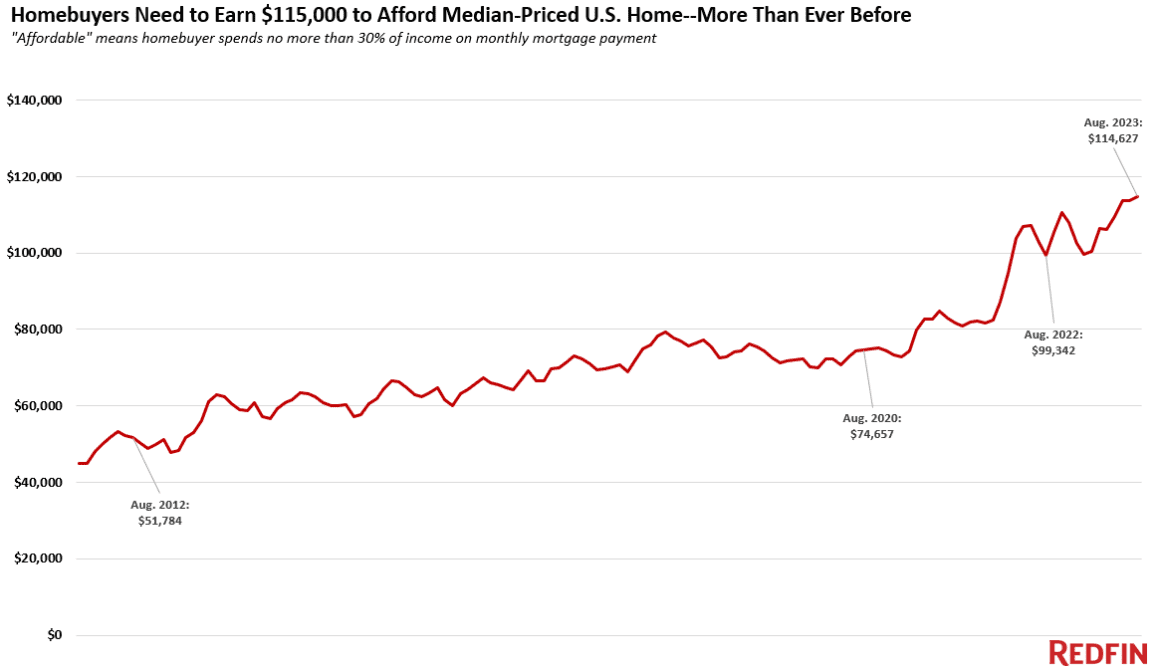

This anti-capitalist meme highlights the spiraling cost of housing since 2012, where the price of a median American home has skyrocketed from under $60,000 to nearly $115,000. It suggests that the rising value of housing acts as a form of structural economic exclusion, where the "affordable" threshold—defined as a home costing less than 30% of income—has become impossible for most workers to reach. The chart visually argues that the dominance of real estate capital values has made homeownership increasingly unattainable for the working class.

simple-description (llama3.2-vision_11b)

The meme is a graph showing the average salary required for a median-priced home in the US, with a red line indicating the average salary for each year from 1990 to 2023. The caption "The average salary needed to buy a home in the US has increased by 53% since 1990, but wages have only increased by 17% in the same time period. " is a commentary on the struggle to afford housing in the US, highlighting the disconnect between rising home prices and stagnant wages.

detailed-analysis (gemma3-27b-vision)

Okay, here's an analysis of the provided graph, broken down into sections corresponding to the requested theoretical frameworks. Note that some frameworks apply more readily than others, and I’ll explain where those limitations are.

I. Visual Description

The graph presents a line chart tracking the income needed to afford a median-priced U.S. home, where "affordable" is defined as not exceeding 30% of monthly income spent on the mortgage payment.

- X-axis: The chart doesn’t explicitly label time, but the points marked as Aug 2012, Aug 2020, and Aug 2023 indicate a timeline over roughly a decade.

- Y-axis: Represents the income in dollars needed to afford a median-priced home, ranging from $0 to $140,000.

- Line: A red line shows the fluctuating income requirement over time. It begins around $51,784 in 2012, gradually increases with some fluctuation until around 2020. After 2020, there's a sharp increase culminating in a peak of about $114,627 in 2023.

- Key Data Points: Specific data points are labeled for August 2012 ($51,784), August 2020 ($74,657), August 2022 ($99,342), and August 2023 ($114,627).

- Overall Trend: The graph demonstrates a clear upward trend, indicating that the income required to afford a median-priced home has significantly increased over the decade, especially in the past few years.

II. Foucauldian Genealogical Discourse Analysis

This framework examines how the concept of “affordability” itself is constructed through discourse, power relations, and historical shifts.

- Power/Knowledge: The graph isn’t simply an objective representation of reality; it is produced by Redfin, a company with vested interests in the housing market. The definition of “affordability” (30% income on mortgage) is a regulatory norm – a social constraint that normalizes a particular economic arrangement. This norm, while seemingly rational, obscures other potential arrangements (e.g., communal living, government-subsidized housing) and reinforces the existing system of homeownership as the desired norm.

- Genealogy of “Affordability”: Tracing the history of “affordability” would reveal how it has been discursively constructed over time, shaped by policies like the 30-year mortgage (itself a product of the New Deal), tax breaks for homeowners, and the narratives surrounding the “American Dream.” The graph performs the normalization of a standard that may not be universally attainable or desirable.

- Disciplinary Power: The graph can be seen as an exercise of disciplinary power. By framing homeownership as a necessary step toward financial stability, it subtly pressures individuals to participate in a system that may be inaccessible to many, creating a "debt economy" wherein individuals are required to borrow money in order to secure this 'dream'.

- Normalization: The graph can be seen as the normalization of an increasing barrier to homeownership. As the graph rises, it suggests that a higher income is simply what's needed, subtly shifting the responsibility from systemic factors to individual earning potential.

III. Critical Theory

This framework analyzes how the graph reveals underlying social and cultural problems.

- Commodification of Housing: The graph highlights the increasing commodification of housing. Housing isn't treated as a basic human right but as an investment vehicle, subjected to market forces and speculative pricing. The line's upward trajectory illustrates the prioritization of profit over access to shelter.

- Alienation: The ever-increasing income requirement alienates large segments of the population from the possibility of homeownership. This creates a sense of exclusion and disempowerment, contributing to social stratification.

- Instrumental Rationality: The graph represents the dominance of instrumental rationality. The focus is on maximizing financial returns, with little consideration for social equity or the well-being of individuals. The algorithm of market forces prioritizes efficiency (profit) over ethics (access to housing).

- Loss of Social Solidarity: The graph can be interpreted as a symptom of a weakening of social solidarity. The emphasis on individual financial success reinforces individualism and undermines collective responsibility for ensuring basic needs are met.

IV. Marxist Conflict Theory

This framework analyzes the graph through the lens of class struggle and economic exploitation.

- Capital Accumulation: The rising income requirement is a direct result of capital accumulation – the concentration of wealth in the hands of a few. Real estate has become a major vehicle for capital accumulation, driving up prices and making it inaccessible to the working class.

- Exploitation of Labor: The graph illustrates how the value produced by labor isn't equitably distributed. Wages have not kept pace with the rising cost of housing, meaning workers are being exploited – they're producing the wealth that drives up housing prices but can't afford to benefit from it.

- Class Stratification: The graph dramatically demonstrates the increasing class stratification in the U.S. Homeownership becomes a marker of privilege, creating a widening gap between the haves and have-nots.

- Ideology: The “American Dream” narrative, which emphasizes homeownership as a symbol of success, functions as an ideology that masks the underlying economic inequalities. The graph can be read as evidence that this dream is becoming increasingly unattainable for many.

V. Postmodernism

- Deconstruction of Grand Narratives: The graph challenges the "grand narrative" of homeownership as a universally desirable and achievable goal. It reveals the constructed and contingent nature of this narrative, demonstrating that it's not based on objective reality but on shifting economic forces.

- Simulacra and Simulation: The graph, as a representation of a complex economic reality, can be seen as a simulacrum – a copy that precedes the original. The graph doesn’t reflect the "real" affordability of housing, but a simulated version created by data points and algorithms.

- Fragmented Reality: The fluctuating line represents a fragmented and unstable economic reality. There is no fixed or universal standard of affordability, but a constant negotiation between market forces and individual circumstances.

VI. Queer Feminist Intersectional Analysis

This framework analyzes how housing affordability intersects with multiple forms of oppression, particularly along lines of gender, sexuality, and race.

- Intersectionality: The graph doesn’t reveal the disparities in housing affordability within the broader trend. For women (particularly women of color), LGBTQ+ individuals, and people with disabilities, the income requirement is likely even higher due to systemic discrimination in wages and employment.

- Gendered Economics of Housing: Historically, women have faced barriers to accessing credit and owning property. This contributes to a wealth gap that makes homeownership even more challenging. The graph obscures these gendered economic realities.

- Racial Wealth Gap: The racial wealth gap in the U.S. is significant, stemming from historical and ongoing discrimination. Black and Latinx families have less accumulated wealth, making it harder to save for a down payment or qualify for a mortgage. The graph doesn’t account for these racial disparities.

- Queer Exclusion: LGBTQ+ individuals may face discrimination in housing, further limiting their access to affordable options. The graph doesn't reflect the unique challenges faced by queer communities.

- Care Work & Housing: The graph fails to acknowledge the disproportionate amount of unpaid care work (childcare, eldercare) performed by women, which limits their earning potential and ability to save for a home.

Limitations:

- Data Specificity: The graph presents a national average. This obscures regional variations in housing affordability and the unique challenges faced by different communities.

- Simplification: The graph only focuses on income as a factor in housing affordability. It doesn't account for other important factors like credit score, debt-to-income ratio, and access to down payment assistance.

I hope this detailed analysis is helpful! Let me know if you'd like me to expand on any of these theoretical frameworks or explore additional connections.

tesseract-ocr

Homebuyers Need to Earn $115,000 to Afford Median-Priced U.S. Home--More Than Ever Before "Affordable" means homebuyer spends no more than 30% of income on monthly mortgage payment $140,000 ‘Aug, 2023: $114,627 $120,000 $100,000 $80,000 Aug. 2022: $99,342 $60,000 ‘Aug. 2020: $74,657 $40,000 ‘Aug. 2022: $51,784 $20,000 ° REDFIN

simple-description (llama3.2-vision)

This meme is a graph that shows the cost of a home in the United States, with a price of $1,000,000 in 2023, and a price of $1,000 in 1973. The text "1/4 of a house for the price of a house" is written above the graph, highlighting the massive increase in home prices over the past few decades. The graph is meant to be humorous, poking fun at the absurdity of the high cost of living in the US.