First Seen

2023-12-17T06:02:40+00:00

simple-description (qwen3.5_2b-q8_0)

The chart satirizes the rapid and unsustainable rise of the "Housing Bubble," illustrating how median mortgage payments exploded from roughly $1,200 to over $2,000 over the years. For someone who cannot see the specific numbers, this represents the terrifying reality of the financial market, suggesting that the rapid growth in values is an unsustainable bubble that the "Anti-Capitalist" view warns is being artificially manipulated by the government rather than reflecting true market stability.

simple-description (llama3.2-vision_11b)

The meme is a chart comparing the median home price in the US to the median income, with a red line indicating the point at which the median home price is no longer affordable for the median household. The chart is captioned "When the median home price is no longer affordable for the median household" and features a red line that says " Median Home Price > Median Household Income". This meme is a commentary on the increasing unaffordability of housing in the US, where the median home price is now higher than the median household income, making it impossible for many people to afford a home.

detailed-analysis (gemma3-27b-vision)

Okay, here's an analysis of the provided graph of median principal and interest payments, framed through the lenses you requested. I'll only include sections where the framework meaningfully applies. I'll prioritize deeper dives into relevant theories and avoid superficial applications.

Visual Description

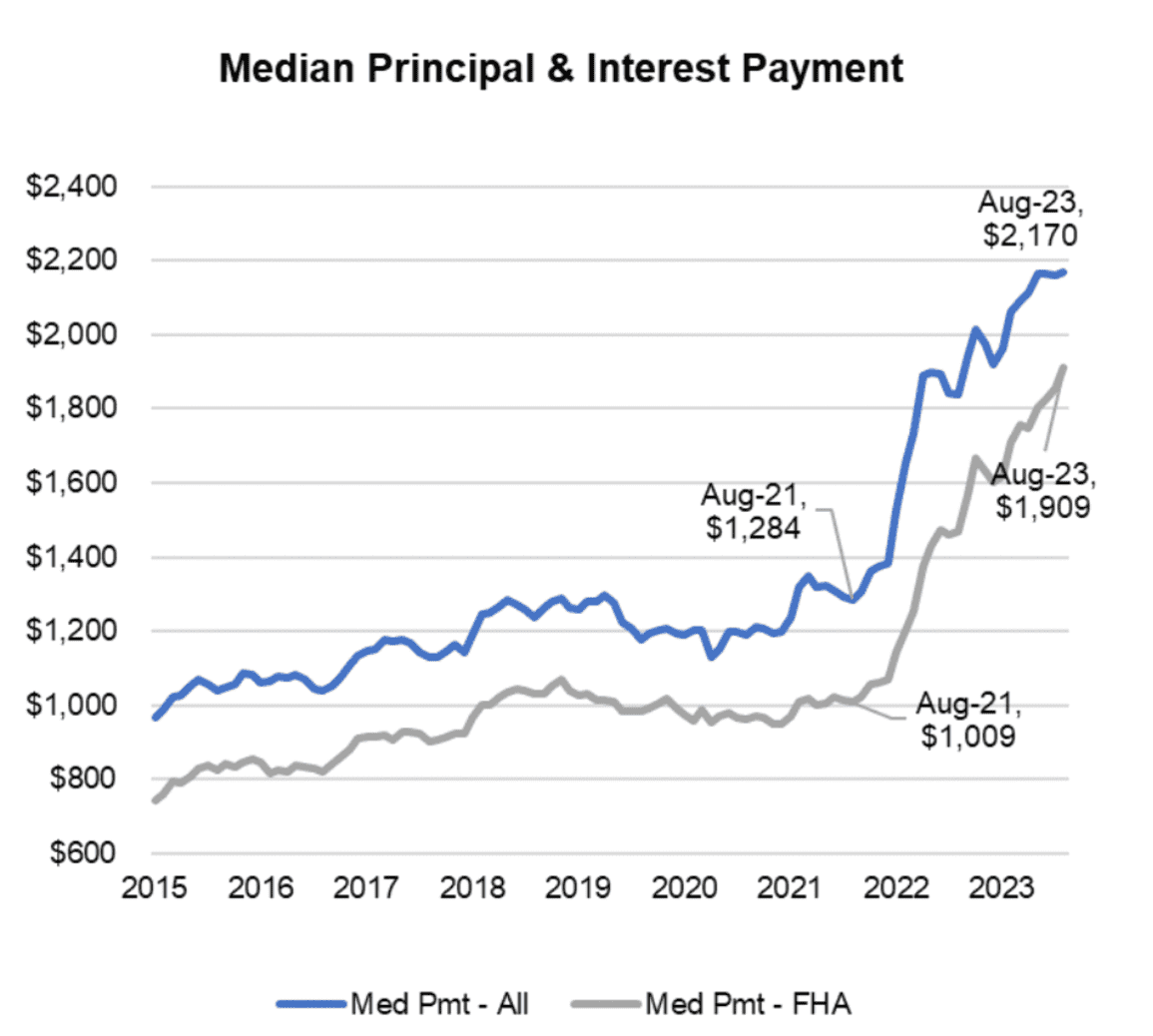

The graph illustrates the trend of median principal and interest payments for home mortgages from 2015 to August 2023. Two lines are presented: a blue line representing all mortgages (“Med Pmt – All”) and a grey line representing mortgages insured by the Federal Housing Administration (FHA) (“Med Pmt – FHA”).

From 2015-2020, both lines demonstrate relative stability, hovering around the $1,000-$1,200 range with some fluctuation. The FHA line consistently remains below the “All” line, indicating generally lower payments for FHA insured mortgages.

A significant upward trend begins in late 2020, accelerating dramatically in 2022 and into 2023. By August 2023, the “All” median payment reaches $2,170, while the FHA median payment reaches $1,909. The gap between the lines narrows, but remains. The late 2023 period shows some volatility in both lines, but the overall trend remains upward. The data points provided at Aug-21 and Aug-23 serve as benchmarks for comparison.

Foucauldian Genealogical Discourse Analysis

This graph, and the economic data it represents, can be understood through a Foucauldian lens as a manifestation of power/knowledge at work in the realm of housing and finance.

- Discourse of Homeownership: The very framing of housing as an essential component of the “American Dream” is a discourse that has been historically constructed and maintained. This discourse isn’t neutral; it encourages certain behaviors, normalizes debt, and positions homeownership as a marker of success and stability. The graph reveals how the conditions for participating in this discourse (being able to afford a mortgage) are changing.

- Discipline of Credit: The entire system of mortgage lending and credit scoring acts as a disciplinary mechanism. Individuals are evaluated, categorized, and subjected to standards (creditworthiness) that regulate their access to housing. The increasing payments, as visualized here, represent an intensification of this discipline – a tightening of the criteria for participating in the system.

- Genealogy of the Mortgage: A genealogical investigation would trace the historical development of the mortgage system itself, from its origins to its current form. This would reveal how specific regulations, financial instruments (like securitization), and political decisions have shaped the terms of access to housing. The dramatic increase in payments starting around 2020 can be connected to specific policy shifts, interest rate adjustments by the Federal Reserve, and the broader financial context (e.g., inflation).

- Biopower and Housing: Housing is intimately linked to biopower (Foucault’s concept of power over life). Access to secure, affordable housing is fundamental to the biological and social reproduction of individuals and populations. Increasing mortgage payments, and the potential for foreclosure, represent a form of biopower – the capacity to control and regulate life through economic and financial means.

Critical Theory

This graph resonates strongly with the concerns of Critical Theory, particularly as it relates to the reproduction of social inequalities.

- Systemic Inequality: The graph doesn’t just show changing housing costs; it reveals the systemic forces that make housing unaffordable for many. The upward trend in payments demonstrates how the system itself is structured to benefit certain groups (those with existing wealth, higher incomes) while disadvantaging others.

- Commodification of Housing: Critical theorists would see housing not as a neutral good, but as a commodity subjected to the logic of the market. The rising payments reflect the prioritization of profit over human needs. The system is geared toward maximizing returns for financial institutions, even if it means making housing inaccessible for a significant portion of the population.

- Ideology of Meritocracy: The discourse of homeownership often implies that anyone can achieve it through hard work and responsible financial behavior. However, the graph challenges this narrative by demonstrating that external economic forces (inflation, interest rates) play a far more significant role. This exposes the ideological function of the “American Dream” – masking the systemic barriers to social mobility.

- Rationalization and Bureaucracy: The mortgage system is a highly rationalized and bureaucratic structure. The graph can be viewed as an indicator of the consequences of this rationalization— increasing complexity, standardization, and ultimately, cost.

Marxist Conflict Theory

From a Marxist perspective, the graph clearly illustrates the inherent contradictions within the capitalist system.

- Class Struggle: The rising mortgage payments represent a form of exploitation. Those who own capital (banks, financial institutions) profit from the increased cost of housing, while those who rely on wages (homebuyers) are burdened with higher debt. This creates a fundamental conflict of interest between different classes.

- Surplus Value: The graph can be understood in terms of surplus value. Financial institutions extract surplus value from homebuyers through interest payments and fees. The increasing payments represent a greater extraction of surplus value.

- Capital Accumulation: The rising costs of housing contribute to capital accumulation in the hands of the financial elite. As more wealth is concentrated in fewer hands, the gap between the wealthy and the working class widens.

- Commodity Fetishism: The graph highlights the alienation inherent in the capitalist system. Housing, a basic human need, is treated as a mere commodity, divorced from its social function. The focus is on profit, not on providing adequate shelter for all.

- Crisis Tendency: The increasing unaffordability of housing could ultimately lead to a crisis of capital accumulation. If people cannot afford to buy homes, it could destabilize the financial system.

Postmodernism

A postmodern lens allows us to critique the universalizing claims about homeownership and financial stability.

- Deconstruction of the "American Dream": The graph deconstructs the idealized narrative of the "American Dream" by revealing its contingent and unstable nature. The rising payments demonstrate that the dream is not accessible to everyone, and that its realization is subject to external economic forces.

- Fragmentation of Experience: The graph can be seen as a representation of the fragmentation of modern experience. The rising costs of housing contribute to a sense of insecurity and instability for many individuals.

- Simulation and Hyperreality: The narrative of homeownership, as promoted through advertising and media, can be seen as a simulation of reality. The graph reveals the gap between this simulated reality and the actual economic conditions faced by homebuyers.

- Rejection of Metanarratives: The graph challenges the idea of a single, unifying narrative about homeownership. It highlights the diversity of experiences and the contingency of economic conditions.

Queer Feminist Intersectional Analysis

This analysis would emphasize how the burdens of rising housing costs are not distributed equally, and are often exacerbated by intersecting forms of oppression.

- Gendered Impact: Historically, women have faced discrimination in access to credit and homeownership. Rising mortgage payments disproportionately impact women, particularly single mothers and women of color, who may have lower incomes and less access to wealth.

- Racial Inequality: Systemic racism has created significant wealth gaps, making it harder for people of color to afford housing. Rising mortgage payments exacerbate these inequalities, further marginalizing communities of color.

- LGBTQ+ Discrimination: LGBTQ+ individuals have historically faced discrimination in housing, including denial of loans and rentals. Rising costs add another layer of vulnerability, particularly for trans and gender non-conforming individuals who may face additional discrimination.

- Intersectionality of Oppression: The graph reveals how various forms of oppression intersect to create unique challenges for certain groups. For example, a Black trans woman may face discrimination based on her race, gender identity, and sexual orientation, making it even harder for her to afford housing.

- Care Work and Housing: The burden of care work (childcare, elder care) often falls disproportionately on women, limiting their ability to earn income and afford housing. Rising costs exacerbate this imbalance.

I hope this in-depth analysis is helpful! Let me know if you'd like me to elaborate on any specific point or delve deeper into a particular theoretical framework.

tesseract-ocr

Median Principal & Interest Payment $2,400 Aug-23, 2,170 $2,200 $ $2,000 $1,800 $1,600 AG ug-23, g-21, $1,284 $1,909 $1,400 $1,200 $1,000 Aug-21, $1,009 $800 $600 2015 2016 2017 2018 2019 2020 2021 2022 2023 ——Med Pmt- All -==Med Pmt - FHA

simple-description (llama3.2-vision)

The meme is a humorous image of a chart showing the median price of a home in the United States, with a dramatic spike in 2022 and a subsequent drop in 2023. The chart is labeled " Median Price of a Home in the US" and the text "We're good" is written above it, implying that the sudden drop in price is a welcome relief. The image is likely being shared to poke fun at the idea that the sudden drop in price is a good thing, rather than a cause for concern.