First Seen

2023-12-17T06:05:12+00:00

simple-description (qwen3.5_2b-q8_0)

This graph visually demonstrates how economic shifts, specifically the shift from high to low mortgage rates, have drastically eroded home buying power. You can see the line starting near $900,000 in 2021 and plummeting to around $500,000 by late 2022. This illustrates that the maximum value of a home you can afford with a $3,000 mortgage is shrinking, leaving many potential buyers with a significantly reduced purchasing capacity in the housing market.

simple-description (llama3.2-vision_11b)

The meme is a graph showing the average price of a house in the United States over time, with a sharp increase in the 2020s. The caption "I can afford a house now" is ironic, as the price of a house has skyrocketed, making it unaffordable for most people. The meme is a humorous commentary on the rising cost of housing and the challenges of affordability.

detailed-analysis (gemma3-27b-vision)

Okay, let's break down this graph through the requested theoretical lenses.

Visual Description

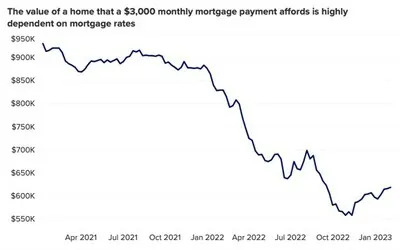

The graph depicts the estimated value of a home that aligns with a $3,000 monthly mortgage payment, plotted over time from approximately April 2021 to January 2023. The y-axis represents the home value in dollars (ranging from $550,000 to $950,000), and the x-axis shows the months.

- Initial Period (Apr 2021 – Jan 2022): The graph begins with a relatively stable, high valuation (around $900k-$950k), showing some fluctuation but overall remaining at a high level.

- Sharp Decline (Jan 2022 – Oct 2022): From January 2022, there's a very significant and rapid decline in home value, falling from near $900k to below $650k within about 9 months.

- Stabilization & Slight Rebound (Oct 2022 – Jan 2023): From October 2022 onwards, the decline slows, and there's a slight rebound, but the value remains significantly lower than the initial levels, settling around $560k-$600k.

Foucauldian Genealogical Discourse Analysis

This graph can be viewed as an artifact within a historical discourse about homeownership, debt, and financialization. Foucault would be interested in the power/knowledge relations at play.

- Genealogy of the $3,000 Mortgage: The graph implicitly traces a genealogy of the idea of a "reasonable" monthly mortgage payment. The selection of $3,000 is not neutral; it's a socially constructed figure based on historical economic conditions, income expectations, and normalized debt levels. Tracing this figure's emergence would reveal how discourses of financial responsibility and "the American Dream" have intertwined with the housing market.

- Normalization of Debt: The graph demonstrates how debt has become normalized as a necessary condition for homeownership. The very framing of home value in terms of a monthly payment reflects this. The decline in value is not just a financial shift but a disruption of this normalized expectation.

- Power and Subjectivation: Discourses around mortgages and housing subjectivate individuals, shaping their identities and life choices. The graph shows how individuals' perceived access to the "good life" is tied to their ability to navigate and conform to the rules of this financial system. The sharp decline could be seen as a moment of disruption in that subjectivation.

Critical Theory

Critical theory focuses on exposing and challenging systems of power and domination. This graph provides a window into the inherent contradictions of capitalism and the way it affects housing.

- Commodification of Housing: The graph reinforces the idea that housing is a commodity subject to market forces, rather than a basic human right. The focus on monetary value obscures the social purpose of housing (shelter, community).

- Financialization of Housing: The graph demonstrates how housing has become increasingly financialized, tied to complex financial instruments and speculation. The rapid fluctuations in value suggest that housing is being treated as an investment vehicle rather than a place to live.

- The Illusion of "Affordability": The selection of a $3,000 mortgage as the defining factor suggests an attempt to define “affordability.” But affordability is a relative concept tied to income levels, wealth distribution, and social safety nets. This graph may obscure the fact that housing is becoming less affordable for many people, regardless of the $3,000 benchmark.

Marxist Conflict Theory

From a Marxist perspective, the graph reveals the inherent class conflict embedded within the housing market.

- Housing as a Site of Exploitation: Housing can be seen as a site of exploitation, where capital is accumulated by landlords, developers, and financial institutions at the expense of working-class individuals and families.

- The Reserve Army of Labor: Declining home values may lead to increased foreclosures and displacement, creating a "reserve army of labor" – a pool of unemployed or underemployed individuals who can be exploited for lower wages.

- Capital Accumulation: The fluctuation in home values represents the shifting dynamics of capital accumulation. The rise and fall of the graph can be interpreted as cycles of speculation and profit-taking by those who control the means of production in the housing sector.

Postmodernism

A postmodern reading of the graph would emphasize the instability of meaning and the fragmentation of reality.

- The Simulacrum: The value represented on the graph is a simulacrum – a copy of a copy – divorced from any intrinsic or real value. It's a symbolic representation based on abstract financial calculations, disconnected from the actual living experience of owning a home.

- Deconstruction of "Home": The graph challenges the traditional, romanticized notion of "home" as a stable, secure, and emotionally fulfilling place. The constant fluctuations in value suggest that homeownership is increasingly precarious and contingent.

- Hyperreality: The graph exists within a hyperreality where the media and financial markets create a sense of reality that is more "real" than real life. The chart itself becomes a part of that hyperreality.

Queer Feminist Intersectional Analysis

This perspective would focus on how the changing housing market impacts marginalized communities.

- Disproportionate Impact: Declining home values can disproportionately harm communities of color, LGBTQ+ individuals, and women, who may have less access to wealth and credit.

- Intersection of Oppressions: The housing crisis intersects with other forms of oppression, such as racism, sexism, and homophobia, creating unique vulnerabilities.

- Housing as a Site of Resistance: Marginalized communities have historically used housing as a site of resistance against systemic oppression, through community land trusts, tenant organizing, and mutual aid networks. The graph can be used as a tool to highlight the urgency of these struggles.

Disclaimer: These are just interpretations, and the "correct" reading will depend on the specific theoretical framework you choose to prioritize. Each perspective offers a different lens through which to understand the complex social and economic forces at play in the housing market.

simple-description (llama3.2-vision)

This meme is a graph showing the value of a home in the United States over time. The text "The value of a home that could be bought for $1,000 in 1970" is written above the graph, implying that the value of a home has increased significantly over the past few decades. The graph shows a steady increase in value until 2022, when it suddenly drops to a much lower value, with the text "2022: $450,000" written below the graph.

tesseract-ocr

‘The value of @ home that a $3,000 monthly mortgage payment affords is highly dependent on morgage rates $9504 900 0804 000% $0801 800% ‘e200 442021 0c1202 Jon2022 Apr 2022 142022 042022 Jon 2023